Farmland at a Crossroads: Ownership, Investment and Use

“Farmland at a Crossroads: Ownership, Investment and Use” ~ PDF

The High Demand for Farmland: Causes and Effects of Increasing Values Across the Midwest

This Issue Brief examines the root causes behind the rapid rise in cropland values relative to growth in yields and net farm income, as well as the implications for rural economies in the Midwest. It also outlines available policy options for states. Five key areas are covered.

- Competing uses for farmland — Societal pressures, such as feeding a growing global population, urbanization and increased housing needs, and the push to expand domestic and renewable energy production, are driving increased demand for farmland.

- Farmland as an investment asset — Farmland held or purchased for investment purposes continues to produce crops and generate revenue for farm operators. However, shifts in who receives farm profits and where those profits are circulated geographically can significantly affect rural communities.

- Farm financialization — Investment by public and private equity firms is on the rise. In states where corporate ownership bans remain intact, institutional ownership is more limited. Farmland held in retirement, acquired through inheritance, or purchased as a personal investment also influences land values. As more farmland is retained for passive income generation, less becomes available on the open market.

- Tax implications — To explore the tax implications for farmland transfers, CSG Midwest analyzed a hypothetical $7 million farm transfer under three scenarios for each Midwestern state, with resulting tax liabilities ranging from a low of $31,500 to a high of $2.02 million.

- Policy options — Several states have developed programs to help beginning farmers access farmland and assist aging farmers with succession planning.

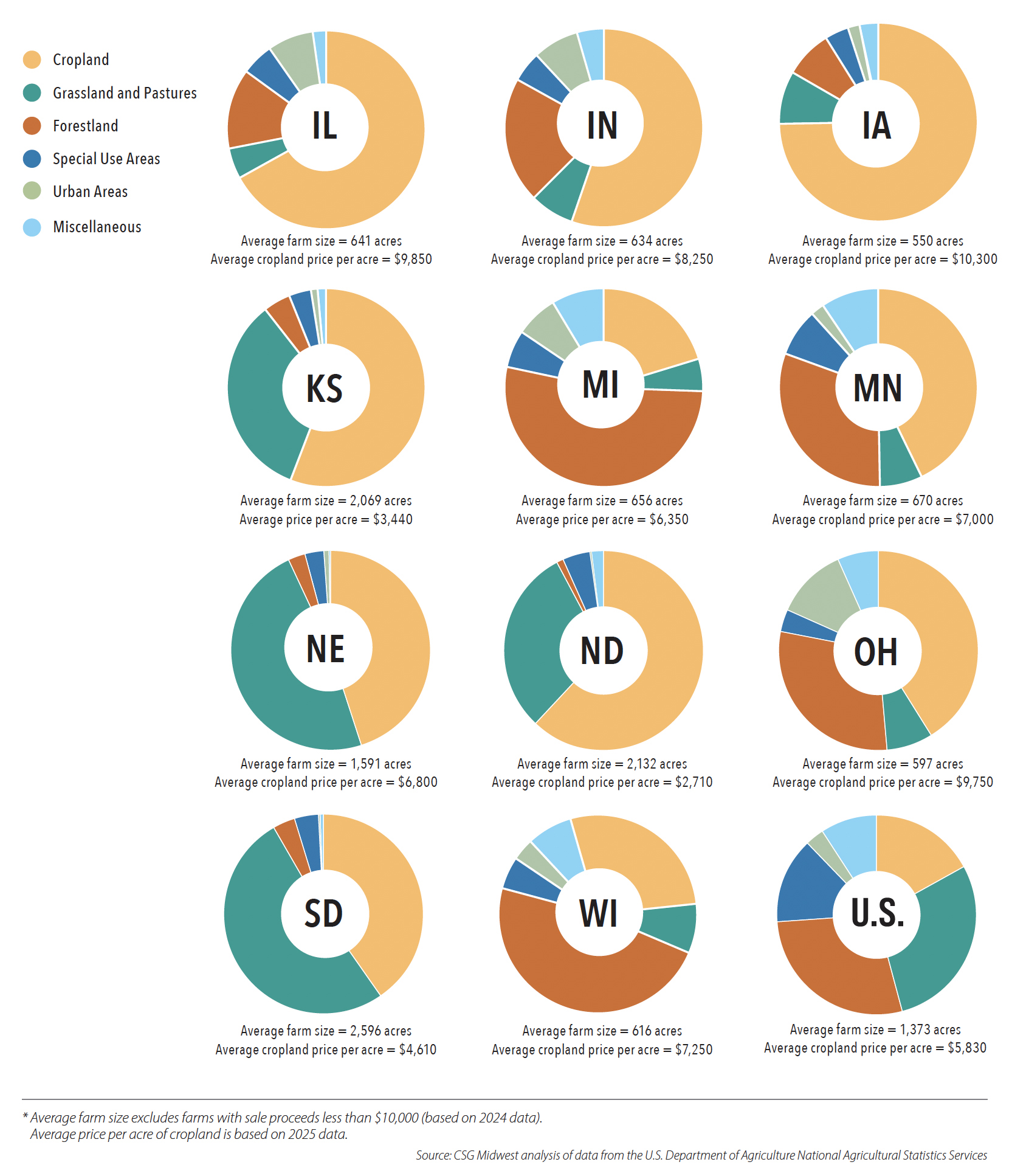

Major Land Uses by State, Average Farm Size and Average Cropland Value*

This Issue Brief was written by Rebecca Leis of the Midwestern Office of The Council of State Governments. It was produced as part of CSG Midwest’s support of two binational, interstate committees of the Midwestern Legislative Conference: and the MLC Agriculture and Rural Affairs Committee.

Trends in Midwest Cropland Values and Net Farm Income *

Urban Land Use by Region: 1945-2017

Farmland in the Midwest

The United States has 876 million acres of farmland. Forty-three percent of it (382 million acres) is dedicated to growing crops that produce food, fuel, feed and fiber. Over half of all U.S. cropland is in the 11-state Midwest region (Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Nebraska, North Dakota, Ohio, South Dakota and Wisconsin).

The productivity of America’s cropland has increased over the last 35 years. Today, U.S. farmers produce 63 percent more tons of corn, soybeans, wheat and sorghum on that same cropland than they did in 1990 thanks to advances in modern farming, such as better seed genetics, weed control and fertilizers.

As yields per acre increased, so, too, did the average price of cropland, but at a much higher rate: Between 1997 and 2024, cropland values in the Midwest increased by approximately 429 percent, rising from $1,246 in 1997 to $6,590 per acre in 2024.

By comparison, since 1997, the change in net farm income has been more modest, increasing 36 percent after adjusting for inflation. The line graph below uses 1997 as an indexed base year to show how cropland values increased relative to net farm income in the 11-state Midwest region.

Land values are rising due to factors beyond yields and farm income — particularly competition for farmland, financialization and tax policies that accelerate consolidation.

Competing uses for farmland

Increased demand for cropland increases its value. Competition for cropland stems from several societal pressures — for example, feeding an increasing global population and boosting domestic and renewable energy production. Competition increases near population centers, too, here urban development drives up demand for farmland and creates potentially lucrative sale opportunities for landowners.

Less apparent, but increasingly significant, is the increasing demand for farmland as an asset class. Farmland held onto or purchased for investment purposes still produces crops and generates revenue for farm operators. What changes with investor ownership is who receives farm profits and where, geographically, those profits are circulated. This shift can mean less of those profits remain in the community where the farm is located.

Domestic Energy Production

In the mid-1990s, as corn yields climbed and dependence on foreign oil raised national security concerns, ethanol production from corn became a key U.S. energy policy. Today, between 35 and 40 percent of U.S. corn is used to make ethanol to meet renewable fuel standards. U.S. Department of Agriculture (USDA) projections indicate that while vehicle electrification may reduce domestic demand for ethanol, increased global demand resulting from renewable fuel standards could provide a potential market for excess U.S. ethanol. The same USDA report also identified sustainable aviation fuel as another future source of ethanol demand. So, although U.S. demand for ethanol may decline with an electrified vehicle fleet, the amount of land dedicated to ethanol production is projected to remain stable.

Similarly, with the introduction of renewable diesel standards in the early 2000s, soybean oil became a primary feedstock for biomass-based diesel. Today, roughly 5 percent of U.S. soybeans are processed into biodiesel and blended with petroleum diesel to fulfill renewable fuel mandates. USDA data illustrates this growing demand: 46 percent of U.S. soybean oil output in 2022-’23 was used in biofuel production, compared with only 1 percent in 2002.

Across the Midwest, significant farmland acreage also is now dedicated to solar and wind production. According to USDA data, between 2012 and 2020, approximately 20,000 wind turbines and 500 industrial-scale solar farms had been installed in the 11-state Midwest. Seventy percent of those solar farms and 94 percent of wind turbines were sited on cropland. On cropland developed into solar farms, 22 percent of land was taken out of production, whereas only 4 percent of land coverage changed on wind turbine sites.

Using crops for fuel or land for energy production adds to the revenue-generation capacity of armland owners. Approximately 3.5 percent of farm owner-operators reported receiving payments for energy production on their operation between 2011 and 2020, according to the USDA. On average, payments were higher in counties with oil and natural gas production ($32,167) than in those with only wind energy production ($17,303).

Urban Development

More farmland also is lost as it gets converted to housing or other types of infrastructure projects, especially when this land is located near population centers. According to the American Farmland Trust, the United States is losing 2,000 acres of farmland a day to other uses, including development. In an eight-state Midwest region, a University of Illinois study calculated the loss of agricultural land to be 1.6 million acres over a 20-year period, equating to 1 percent of all agricultural land in the region.

When farmland is diverted to alternative uses or lost altogether, this heightens demand for the acres that remain in use for food production. However, not all competition for, or interest in, farmland takes it out of production.

In Demand as an asset class

Like all real estate, farmland is an asset. An asset becomes financialized when it is valued more for its ability to produce wealth through appreciation, portfolio diversification and income generation, rather than through its productive capacity or practical use — just as there are instances in which housing becomes an investment vehicle for the property owners rather than a home.

Over the last 40 years, farmland has shifted from predominantly being owned and operated by the same person to being owned by one individual and being operated by another. With this shift, rental income stays with the owner while the revenue generated from selling a crop is retained by the operator or farm manager. When these income streams are separated, ownership decisions may become more closely aligned with investment considerations than with agricultural productivity.

This financialization occurs primarily among two different spheres of ownership: (1) ownership by institutional investors, including public and private equity firms; and (2) private individual ownership of farmland held onto in retirement, acquired through inheritance, or purchased as individual investments.

The impacts of institutional ownership may vary depending on the strength of a state’s corporate farming laws. In Illinois, Indiana, Michigan and Ohio, institutional investors are permitted to own farmland, while other states in the Midwest have laws designed to limit or prohibit corporate ownership. The efficacy of these laws may be limited in scope, though, depending on the statutory language or past successful legal challenges to them.

Institutional Investors

Farm Financialization: Institutional Investors

Institutional investors are large organizational entities (such as pension funds, endowments and insurance companies) that pool and invest money on behalf of others. The number of farmland properties owned by the seven largest institutional investors in the U.S. increased 231 percent between 2008 and 2023, and the value of those holdings rose more than 800 percent, to around $16.2 billion, according to a 2023 investigation by Reuters.

André Magnan, a University of Regina sociology professor who studies farm financialization, explains that agricultural land is increasingly viewed as a smart asset because “[it] is considered a hedge against inflation, and investors believe that with a growing world population, there will be increasing demand for food.”

In the Midwest, bans on corporate farmland ownership in North Dakota, South Dakota and Minnesota preclude ownership by pension funds, investment funds and public trusts. However, Kansas’ orporate farming ban is silent on the issue. In Wisconsin, domestic corporations and trusts may own farmland or carry out farm operations, provided there are 15 or fewer shareholders (lineal relatives count collectively as one shareholder), and there cannot be more than one family shareholder unit in a single corporation or trust. In Iowa, authorized trusts comprised of less than 25 beneficiaries may own up to 1,500 acres of farmland and may own even more if it is leased to the previous owner.

According to the National Council of Real Estate Investment Fiduciaries, the total value of land owned by big institutional investors is around $16 billion. The U.S. Department of Agriculture estimates the cumulative value of U.S. farmland at $3.4 trillion. Land owned by big institutional investors, then, would equate to roughly one-half of 1 percent of that total. Though seemingly small, investor ownership has the potential to last indefinitely.

Duration of Ownership

When institutional investors purchase farmland, they can hold it indefinitely because corporations do not have a natural endpoint. Without a built-in requirement to dissolve or transfer assets, corporate ownership can lead to long-term consolidation and reduce the amount of farmland available for purchase.

Traditionally, individually owned farmland transfers to the next generation according to the owner’s will or (in the absence of a will) intestate laws. However, many landowners now place farmland in trusts — legal arrangements that manage assets on behalf of beneficiaries under terms set by the grantor. State law limits the duration of such trusts through what’s known as the rule against perpetuities.

The rule against perpetuities restricts the length of time a landowner may direct the use of assets held in trust after death, traditionally capping it at “lives in being plus 21 years.” Most states later codified this into a fixed period of 90 years beyond the owner’s death.

Over the past four decades, though, many states have modified or repealed their rules. South Dakota was the first, abolishing the rule against perpetuities in 1983 and creating a niche market for “dynasty trusts.” These trusts can manage wealth indefinitely without risk of termination, giving South Dakota a competitive advantage in the trust industry.

Since then, many states have relaxed or repealed their perpetuity rules to attract or retain trust business. Illinois, Michigan, Nebraska and Ohio have eliminated the rule entirely. Iowa, Kansas and Wisconsin still follow the Uniform Statutory Rule Against Perpetuities (90 years), while North Dakota retains the traditional “lives in being plus 21 years” standard.

In 2024, Indiana extended its perpetuity period to 360 years upon enactment of HB 1209. Minnesota followed in 2025, setting its limit at 500 years with the passage of SF 571.

The length of the perpetuity period matters less in states with corporate farming bans, which generally prohibit trusts from owning farmland. In contrast, states without such bans or a perpetuity limit, such as Illinois, Michigan, Nebraska and Ohio, allow trusts to hold farmland indefinitely. Indiana permits ownership for up to 360 years.

While trusts may not always retain farmland indefinitely, the ability to do so could limit the future availability of farmland.

Private Ownership

Farm Financialization: Private Ownership

With 84 percent of U.S. farmland owned by private individuals or family farm entities, the more significant driver of farmland financialization comes from land retained by retiring farmers for income or passed down through inheritance.

To a lesser extent, financialization occurs through private investment. Although most owners have personal or family ties to their land, a small share of farmland is purchased by private and sometimes well-known investors. These transactions may draw media attention but represent only a minor portion of total ownership compared with the vast holdings of retirees and farming heirs.

Percent of Land in Farms Rented to Others (2022)

Land held for retirement income

As more farmland owners retire, or transfer their land to the next generation, a greater proportion of their land gets leased to others. This has been a persistent shift over time, especially within the Midwest, where farmland is almost entirely cropland. So, while the total amount of U.S. rented/leased farmland has remained steady, around 39 percent for the past 50 years, in many counties in the Midwest, more than 60 percent of farmland is rented today.

Iowa State University’s 2022 “Farmland Ownership and Tenure Survey,” the longest state-based land survey in the country, further demonstrates this shift in owner status.

In 1982, 55 percent of Iowa farmland was owner-operated. In 2022, just 35 percent was owner-operated. Over the same period, cash-rent leases increased from 21 percent to 56 percent.

The “Tenure Survey” also shows a decline in crop-share leases. In 2022, just 8 percent of all leases were crop-share leases — structured such that the owner and tenant share the expense and/or income of the crop each year. In contrast, with cash rent, the tenant assumes all the risks of production; the landowner simply collects rent.

And, from a tax standpoint, rental income is treated as ordinary income, which generally benefits retirees who are typically in lower income-tax brackets. Treatment of rental income as ordinary income is also important when contrasting it to proceeds from a sale, which is taxed at the capital gains rate.

Distribution of Iowa Farmland by Tenure

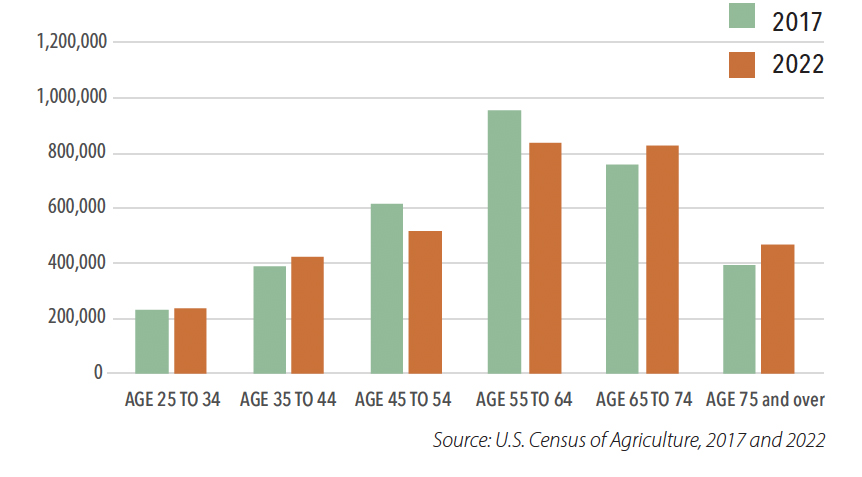

U.S. Farm Operator Age Distribution

The decrease in owner-operator status matches the trend of an increasing age of farmers and landowners. Over the past five years, the number of U.S. farmers over age 65 grew by 12 percent.

The “Tenure Survey” found that 66 percent of farmland in Iowa is owned by individuals age 65 o older, including a record-high 37 percent held by owners over 75. More than 3 million acres, representing 13 percent of Iowa’s farmland, is owned by women over 80. In contrast, in 1982, only 29 percent of Iowa farmland was owned by people 65 or older.

With this shift toward fewer owner-operators and more cash-rent leases, the income generated by crop production is split between two households or balance sheets rather than one.

Financial impacts of splitting farm income

When land is owned and operated by the same individual, that farmer can leverage the land to create fluidity in the overall farm operation. When farmland is cash-rented, the payment is an expense to the operator and benefits the owner who may live hundreds of miles from the farm, circulating the rental income in communities detached from the source of the farm generating the revenue. For example, in North Dakota, non-operating landlords live, on average, 420 miles from the rented farmland, the highest average distance among the 50 states. In Iowa, 23 percent of all leased farmland is owned by those who do not live in the state.

The composition of farmland ownership structures and farm financial viability was recently analyzed by a team of University of Illinois economists. They found that under current economic conditions (low commodity prices), farmers who own a larger portion of their total farm operation had positive net income. As ownership was reduced or more land was cash-rented, farm operators had lower net farm income. Their modeling predicted significant losses for farmers who did not own any farmland and instead were the operators of cash-leased farmland.

Land passed on to heirs

As retired farmland owners pass away, their land will be transferred to new owners according to their succession plans. The American Farmland Trust notes that 371 million acres, 41 percent of U.S. farmland, will change hands by 2035.

Just as elderly landowners are less likely to farm the land they own, so, too, are those who inherit the land. In 2014, more than 50 percent of non-operator landlords obtained their land through inheritance.

Iowa State University’s “Tenure Survey” shows that most farmers in that state intend to pass land to their heirs through a will or trust. Of those surveyed, only a few — representing just 4 percent of Iowa farmland — expected to sell their land to non-family buyers.

Tax policy strongly influences whether landowners will retain or sell farmland in their retirement years. Current policy incentivizes retention.

If more owners choose to hold onto their land, the supply of farmland on the market shrinks. According to Iowa State University’s “2024 Land Values Survey,” landowners identified limited land availability as the leading factor pushing up farmland values.

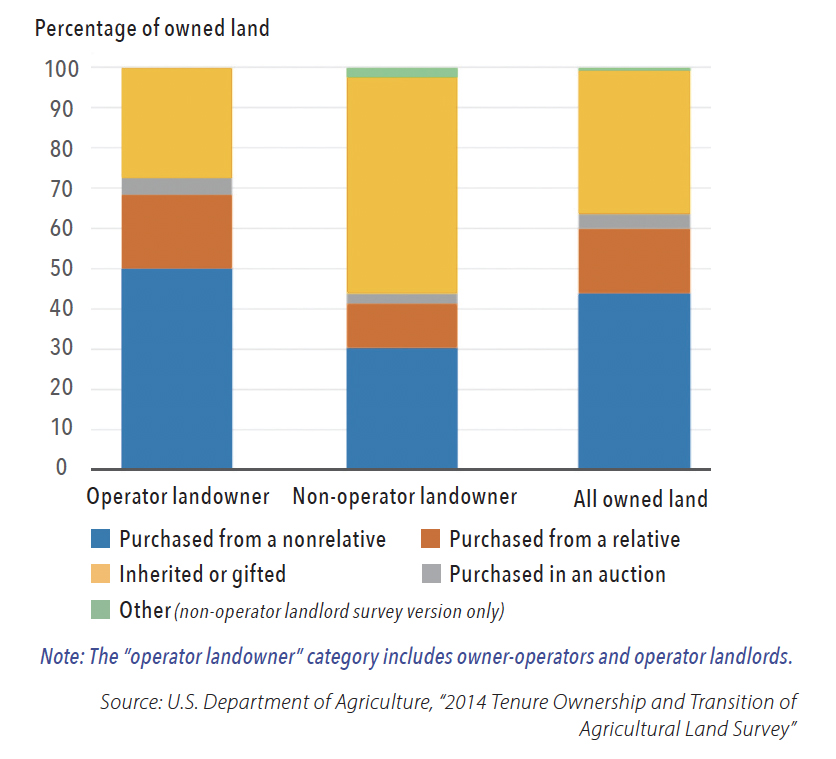

Sources of Acquired Farmland by Tenure

Tax implications of selling and transferring farmland

Several types of state and federal taxes apply to farmland transfers, including capital gains taxes, estate taxes, and inheritance taxes, along with the tax rule known as “stepped-up basis.”

To better understand the tax policy implications, CSG Midwest analyzed a hypothetical $7 million farmland transfer under three scenarios: (1) during the owner’s lifetime, (2) at the owner’s death, and (3) upon the sale of inherited land one year later. A $7 million farm was selected because it reflects a typical Midwestern farm size with revenue likely sufficient to support a full-time farmer without off-farm income.

The tax liability table (below) summarizes the results and the potential tax implications for each state in the Midwest. The analysis shows that the total state and federal tax liability involving this transfer could range from as high as $2.02 million to as low as $31,500.

The state-level variation largely reflects differences in capital gains, inheritance and estate tax policies. Overall, however, current tax structures tend to discourage land transfers made during an owner’s lifetime.

Status of Estate and Inheritance Taxes in the Midwest

Capital Gains Tax and Farmland

When farmland is sold for a profit, the seller realizes a capital gain. Although no sales tax applies, land held for more than one year is subject to a long-term capital gains tax on the profit, which is the difference between the sale price and the original purchase price (adjusted for improvements). Capital gains taxes are collected at the federal level and, in many cases, at the state level as well.

At the federal level, capital gains rates are determined by taxable income. For 2025, married couples filing jointly are subject to the top capital gains rate of 20 percent when their taxable income (including gains) exceeds $600,000. In addition, they may owe the 3.8 percent Net Investment Income Tax on net investment income above $250,000.

Most states also tax capital gains, with the rate typically tied to the state’s income tax brackets. In 2025, the top rates in the 11-state Midwest ranged from 9.85 percent in Minnesota to 2.5 percent in North Dakota. South Dakota has no income tax or capital gains tax.

To reduce the tax burden on farmers, some states provide partial or full exemptions. Iowa, for instance, exempts capital gains on farmland sold to relatives or on land used in a farming business. Wisconsin allows a 60 percent deduction on gains from qualified farm sales.

At the federal level, a new law (H.R. 1 of 2025) now permits taxes on capital gains from qualified farmland sales to be paid over four years instead of all at once. This policy change allows sellers to earn interest on sale proceeds while paying in installments, thereby easing the tax burden.

In the hypothetical case involving a $7 million farmland sale, the federal capital gains tax was $1.428 million. The state capital tax gains varies widely. See the table below.

Estate, inheritance taxes and farmland

When farmland is transferred pursuant to a will, trust or intestate succession, estate and inheritance tax obligations may apply. An inheritance tax is paid by an heir upon receiving property, while an estate tax is paid based upon the total value of a decedent’s assets. The estate pays the tax before assets are distributed.

There is no federal inheritance tax, but several states impose one. Nebraska is the only Midwest state that still levies an inheritance tax. (Multiple measures to repeal it have been introduced but never passed.) Iowa’s inheritance tax was fully repealed on Jan. 1, 2025, following a phase-out that began with the passage of SF 619 in 2021. Within the past 15 years, Indiana and Ohio are among several states nationwide that eliminated their inheritance or estate taxes.

At the federal level, as of 2025, estates valued under $13.99 million per individual (or $27.98 million per couple) were exempt from the estate tax. This exemption is portable, allowing a surviving spouse to use any unused portion of their partner’s exemption. Beginning in 2026, the exemption increases to $15 million, indexed for inflation. According to the Urban-Brookings Tax Policy Center, only about 7,130 estates nationwide are large enough to trigger the federal estate tax.

In the Midwest, only Illinois and Minnesota levy state-level estate taxes. Illinois exempts the first $4 million of an estate, though this exemption is not portable between spouses. Minnesota provides a general $3 million exemption (not portable), which increases by an additional $2 million if farmland passes to a relative who continues to use it for farming.

In the hypothetical case outlined in the table below, the transfer of farmland to an heir generated a tax liability of $638,000 in Illinois (estate tax), $260,000 in Minnesota (estate tax) and $69,000 in Nebraska (inheritance). No other Midwestern states have an estate or inheritance tax.

Steppped-up basis and farmland

Stepped-up basis is a federal tax rule that often reduces or eliminates capital gains taxes when property is transferred at death. It does so by resetting the asset’s cost basis — the original purchase price plus improvements — to the property’s fair market value at the time of the owner’s death. Because the property’s value and its cost basis are the same, no capital gain is realized, and no tax is owed when the property transfers to an heir.

This provision has long helped families keep farmland intact across generations. Without it, many heirs would have been forced to sell portions of inherited property to pay taxes on unrealized gains.

However, over time, ownership becomes further removed from the original farming heirs. Stepped-up basis enables later generations to maintain income-producing farmland without triggering taxes that might otherwise encourage its sale. According to Iowa State University’s “2022 Land Values Survey,” 29 percent of Iowa farmland owners reported having no farming experience.

In the hypothetical example outlined below, when an owner dies, the land’s fair market value becomes the heir’s new cost basis. If the heir sells the land immediately for that value, no taxable gain occurs. A sale one year later illustrates the lasting advantage of the stepped-up basis: even if the land appreciates slightly, the taxable gain, and therefore the tax liability, is minimal.

Competition for farmland as an asset class increases the value because it builds demand. Tax law, meanwhile, discourages large portions of farmland from ever being sold on the open market, thus limiting supply. For current and prospective producers, this means there are fewer opportunities to purchase land.

While most modern farm operations have a combination of owned and rented farmland, farmers need to own a significant portion of it to leverage their farmland in order to secure production loans.

Farmland transfers and their tax implications

Tax liabilities on the sale/transfer of farmland valued at $7 million under three diferent scenarios (see below for details)

![]()

A state-by-state analysis of Midwest tax implications for three farmland transfers

To analyze the implications of different types of transfer, CSG Midwest analyzed the tax laws in each state, as well as the federal government, and used a common scenario predicated on these assumptions:

- The farmland being transferred is valued at $7 million and jointly owned by a retired couple. They have leased the land to their child for five years and are not actively engaged in the farm’s operation. The transfer occurs in 2025.

- The land was purchased in 1995 for $1 million and no improvements were made to the land.

- Here are three options for this transfer of farmland:

Land transferred during owner’s lifetime: While still alive, the husband and wife sell the farmland for $7 million to their only child, who is a farm operator. The sale generates $6 million in realized gains for the husband and wife, triggering a long-term capital gains tax liability – which applies to profits from the sale of an asset held for more than one year. The profits yield the highest federal capital gains tax rate of 20 percent along with the Net Investment Income Tax of 3.8 percent and the highest state capital gains tax rate. The federal capital gains tax of $1.428 million is the same in each state.

Land transferred upon the owner’s death: The transfer at death is from the last remaining spouse to an heir who is the decedent’s only child (married and a farm operator). There is no capital gains tax because stepped up basis applies. At death, the heir’s cost basis becomes the decedent’s costbasis (the original purchase price). The estate is less than

the federal exemption amount of $26 million for married couples in 2025. Therefore, there is no federal estate tax due, but state inheritance and estate taxes apply.

Land sold one year after inheritance: Exactly one year and one day after inheriting the land, the child sells the farmland. During the course of that year, the land appreciates 3 percent (increasing the farmland value to $7.21 million). The sale causes a long-term capital gains tax liability, but stepped-up basis reduces the gain from $6 million to $210,000.

Summary of taxation table:

The transfer of farmland could generate a tax liability as high as $2.019 million or as low as $31,500 depending on which state the land is in, whether the original owner is deceased or living, and, to a lesser extent, if the purchaser is a qualified farmer or a relative who is eligible for a tax reduction.

The state-by-state variability in tax liability is due to state policies on capital gains taxes, inheritance taxes and estate taxes. But across the board, the biggest difference in tax liability involves when the farmland is transferred. As the summary table shows, the amount of taxes owed is much higher when the land is transferred during the owner’s lifetime. The amount is much lower if the transfer occurs after the owner’s death.

Policy Options to increase farmland access

Various state laws and programs, along with partnerships between federal and state governments and the private and nonprofit sectors, aim to increase farmland access to new and beginning farmers. These programs generally fall within three categories: loan programs, tax credits and succession planning.

Beginning farmer loan programs

Federal programs

Throughout the country, the U.S. Department of Agriculture’s Farm Service Agency (FSA) provides lending services to beginning farmers, operators facing financial setbacks, or those with sound business plans but limited collateral. Programs include direct farm ownership loans, down-payment assistance for first-time buyers, direct and micro-operating loans for working capital needs, and guaranteed loans that reduce lender risk.

State programs: Aggie Bonds

Many Midwestern states supplement federal FSA programs with Aggie Bonds, which are federally funded and administered by state agencies in partnerships with traditional lenders. These bonds make interest earned by investors or lenders exempt from federal and, sometimes, state income taxes. Consequently, lenders are willing to accept lower interest rates; borrowers benefit by securing below-market loans. Illinois, Iowa, Indiana, Kansas, Minnesota, Nebraska, North Dakota and South Dakota administer Aggie Bonds, though the terms and conditions vary by state.

Other state-based beginning farm loan programs

For 40 years, Wisconsin’s Housing and Economic Development Authority has assisted farmers looking to borrow funds to purchase machinery, equipment, buildings, land or livestock without the backing of the Aggie Bond program. Wisconsin’s state-based program guarantees loans made by commercial lenders, but caps loans based upon the loan’s purpose and available collateral.

Ohio’s AG-LINK program has operated for more than 30 years, providing farmers, agribusiness and co-operatives with a 3 percent rate reduction on new or existing operating loans. Minnesota’s Rural Finance Authority administers the Aggie Bond program plus other programs such as down-payment grants (up to $15,000) and loans used to help farmers restructure debt or make farm improvements. These state programs require periodic replenishment. To address expected shortfalls by summer 2026, Minnesota’s HF 770 seeks $30 million from the state’s bondproceeds fund to replenish them. The bill remains pending for the 2026 session.

Illinois, Iowa, Kansas, Nebraska and North Dakota also offer state-based beginning farm loan programs designed around similar criteria as those in Wisconsin, Ohio and Minnesota.

Tax credits

Recognizing the barrier to entry created by high land values and limited opportunities to purchase farmland, Iowa, Minnesota, Nebraska and Ohio developed tax credits that support beginning farmers. Nebraska’s program started in 1999 (providing $19.7 million in credits through 2025), whileOhio’s began in 2022. These initiatives generally provide tax credits for existing farmers who lease or sell agricultural land or equipment to qualified new farmers. Although the programs vary, several key features stand out:

- Net worth threshold: All four states cap the net worth of eligible beginning farmers, ranging from $750,000 in Nebraska to $1.042 million in Minnesota.

- Higher tax credit amount for crop-share leases: The programs in Minnesota and Nebraska provide asset owners with a tax credit equal to 10 percent of annual cash-rental income or 15 percent of the crop-share rental income. Iowa’s program is similar, but the tax credit amount is 5 percent of cash-rents and 15 percent of crop-share rents. Ohio’s tax credit does not distinguish between the type of rental agreement. The asset owner receives a tax credit that is 3.99 percent of the sale price or of the gross rental income received in the first three years of a lease.

- Ability to farm: All four states require beginning farmers to demonstrate their interest and ability to farm based upon training or experience, and some require enrollment in a farm management program. • Relation to the asset owner: Nebraska’s and Minnesota’s programs include caveats regarding when and how tax credits can be obtained if the asset owner is also related to the beginning farmer. Iowa’s and Ohio’s programs do not expressly permit or deny the benefit based upon familial relations.

In August 2025, Illinois enacted SF 2372, which creates a commission within the state Department of Agriculture. It will examine barriers faced by individuals ages 25 to 40 looking to purchase farmland. The commission will then make recommendations to improve state-level supports.

Succession Programs

Every Midwestern state offers succession planning workshops to assist farmers and rural landowners in developing estate and succession plans. Programs tend to be offered by land-grant universities and have funding from a mix of state, federal and county appropriations.

The user cost, length and breadth of programming, and willingness to meet with individual families varies by state.

Farm link programs

Not all farms have a successor and not all prospective farmers have access to farmland. For those situations, many states fund programs that connect unrelated farmland owners with farmers looking to buy or lease land. The American Farmland Trust provides a directory of farmland matching programs. Ten programs serve the following Midwest states: Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Nebraska, Ohio and Wisconsin, according to the American Farmland Trust.

With the introduction of AB 411 and SB 412 in 2025, the Wisconsin Legislature is considering measures to codify a farm link program in statute.

Conclusion

The steady appreciation of farmland values across the Midwest reflects a convergence of powerful social, economic and policy dynamics. Farmland is no longer valued simply for its productive capacity, but increasingly as a financial asset that generates income, diversifies portfolios and serves as a hedge against inflation.

A considerable amount of farmland also never goes up for sale, due in part to tax policies that encourage owners to retain the land even as they age and retire. The land is passed on to heirs.

This limits the amount of land available for new and beginning farmers to purchase, a challenge compounded by the loss of farmland to urban growth and use for energy-related production.

Together, all these forces have made farmland an increasingly scarce resource that is a highly sought-after asset, driving prices beyond what farm productivity or income growth supports alone. While rising land values can strengthen rural wealth and balance sheets, they also threaten the accessibility and long-term sustainability of agricultural production.

The growing separation between ownership and operation means fewer opportunities for new farmers and less local reinvestment of farm income. Policymakers seeking to rebalance farmland markets may look to strengthen beginning farmer tax credit programs, expand capital gains relief for qualified farm sales, and examine the long-term implications of corporate ownership and perpetuity laws that enable indefinite land retention.

Ensuring that farmland remains both a productive resource and a viable economic foundation for future generations will require deliberate coordination in agricultural, tax and land-use policy.